FX Daily Strategy: N America, April 24th

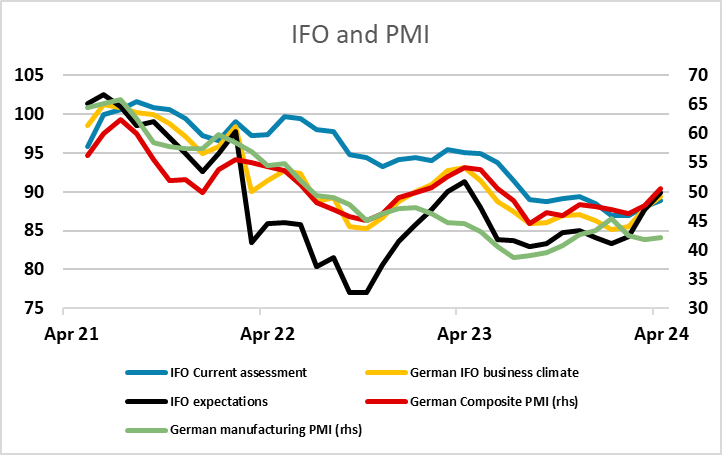

IFO needs to beat consensus to justify EUR/USD strength

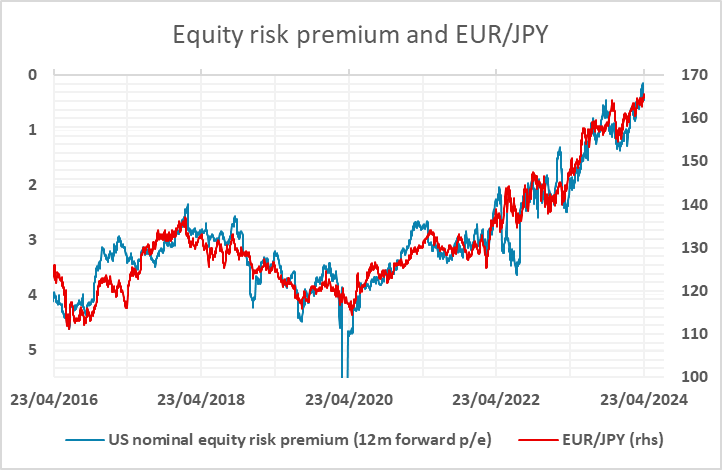

EUR/JPY move to new highs may be temporary

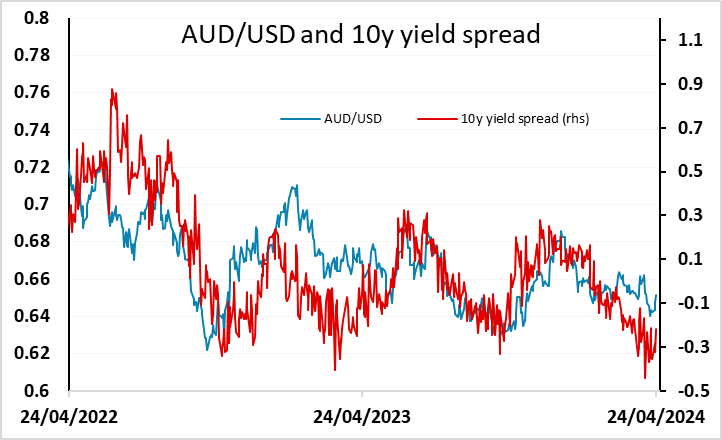

Hotter CPI to Support Aussie in a Short Run

IFO beats published consensus, but fails to boost EUR

EUR/JPY move to new highs may be temporary

Hotter CPI to Support Aussie in a Short Run

IFO was slightly stronger than the published consensus, but probably broadly in line with market expectations after the stronger than expected S&P PMIs yesterday. EUR/USD blipped slightly higher on the release but subsequently resumed the modest declining trend seen through the earlier part of the morning, with front end German yields not noticeable affected. It still looks hard for EUR/USD to advance beyond 1.07 until or unless there is some other data to support the relatively weak US PMIs seen on Tuesday.

The EUR (and GBP) also made gains against the JPY on Tuesday as a consequence of the weaker US numbers and the stronger numbers in Europe. Of course, the Japanese PMI data was also strong, but no-one pays attention to that. The strength of EUR/JPY typically reflects positive global risk appetite rather than any specific economics, and the equity market gains after the US data consequently helped EUR/JPY to break above 165 hitting new 16 year highs at 165.75. But as we have noted before, EUR/JPY doesn’t typically follow equity indices, but rather reflects moves in the equity risk premium. Equity gains based on lower yields consequently don’t typically have a sustained positive impact. However, if anything EUR/JPY has been lagging behind the decline in equity risk premia of late, so at this stage we wouldn’t expect a significant turn lower in EUR/JPY unless the BoJ decide that enough is enough and it’s time to intervene. We doubt this will be the case unless USD/JPY also recovers and makes new highs above 155.

Riskier currencies continued to perform well overnight, with the AUD in particular doing well after stronger than expected Australian Q1 CPI. This had the effect of completely eliminating market expectations of RBA easing this year. The curve now looks for rates to remain unchanged through the year. AUD yields are higher along the whole curve, but even so, yield spreads with the USD are not suggesting further significant AUD gains at this point. The recovery in risk and the rise in AUD yields ought to mean that the low end of the range below 0.64 is now out of reach for the foreseeable future, but it is still likely to require lower yields in the US if AUD/USD is to press towards this month’s highs above 0.66. For now, a mild upside bias should persist, but we are likely to remain closer to 0.65 than 0.66.